Bitcoin vs blockchain

blockchain for beginners

blockchain healthcare

blockchain pros and cons

blockchain real-world applications

Blockchain security

blockchain supply chain

blockchain technology explained

blockchain use cases

blockchain vs database

decentralized ledger technology

distributed ledger benefits

how blockchain works

smart contracts explained

what is blockchain

Coinposters

What is Blockchain Technology? (Pros & Cons) Plain-English Explainer for Beginners & Students

BEGINNER’S GUIDE · BLOCKCHAIN TECHNOLOGY · CRYPTO BASICS

Article At A Glance

- Understanding blockchain technology explained: Blockchain is a digital record-keeping system that stores information in linked blocks across thousands of computers simultaneously—making it nearly impossible to alter or hack

- It goes far beyond Bitcoin—blockchain is actively being used in healthcare, supply chains, banking, and identity verification right now

- The biggest advantages include decentralization, security, transparency, and cutting out expensive middlemen like banks

- The real drawbacks—including energy consumption and slow transaction speeds—are often glossed over, and we cover them honestly here

- You don’t need to own cryptocurrency to interact with or benefit from blockchain technology

Table of Contents

- Blockchain Is Simpler Than You Think

- What Problem Does Blockchain Solve?

- How Blockchain Actually Works

- The Pros of Blockchain Technology

- The Cons of Blockchain Technology

- Where Blockchain Is Used Today

- Bitcoin vs. Blockchain: They Are Not the Same Thing

- Is Blockchain the Future or Just Hype?

- Frequently Asked Questions

Blockchain sounds complicated, but once you strip away the technical language, it’s one of the most logical ideas in modern technology.

If you’ve ever tried to understand what blockchain technology explained actually means—beyond “it’s what Bitcoin runs on”—you’re in the right place. This guide breaks it down from the ground up, covers the honest pros and cons, and shows you where it’s already changing real industries.

Blockchain Technology Explained: Simpler Than You Think

Most people hear “blockchain” and picture something reserved for computer scientists or Wall Street traders. The reality is far more approachable.

What Blockchain Actually Is (No Jargon)

A blockchain is a type of database—but instead of storing data in rows and columns like a traditional spreadsheet, it stores data in blocks that are linked together in a chain. Each block holds a set of records, a timestamp, and a unique code that connects it to the block before it. Once a block is added, it cannot be changed without changing every block after it—which is what makes the system so secure.

Think of it like a shared Google Doc that thousands of people can read, but nobody can quietly edit without everyone else noticing. That’s the core idea.

The Simple Definition

A blockchain is a shared database stored on thousands of computers at once, where every change is visible to everyone and permanent records cannot be altered without the entire network detecting it.

Why It Matters Beyond Bitcoin

Bitcoin was the first major application of blockchain, but the technology itself is not a currency—it’s infrastructure. The same way the internet powers email, shopping, and video calls, blockchain is a foundation that can power many different things. Today it’s being used to track shipments, store medical records, verify identities, and run contracts automatically without lawyers or banks involved. For a deeper understanding of how blockchain is transforming finance, explore the comparison between DeFi and traditional finance.

The potential here is genuinely broad, which is why governments, hospitals, and Fortune 500 companies are all investing in it—not just crypto traders.

What Problem Does Blockchain Solve?

To appreciate what blockchain does, you first have to understand what was broken before it existed. For a deeper dive into the intricacies of blockchain, you might want to explore this beginner guide on DeFi vs Traditional Finance.

The Flaw in Traditional Record-Keeping

Every major institution—banks, hospitals, governments—keeps records in centralized databases. That means one organization controls the data, one organization can change it, and one breach can expose or destroy everything. In 2017, the Equifax data breach exposed the personal information of 147 million people—all because their records lived in one place.

Centralized systems are efficient, but they are also single points of failure. If the central server goes down, gets hacked, or the organization operating it acts dishonestly, everyone who depends on that data is vulnerable.

Why Banks and Middlemen Are the Old Way

When you send money to a friend through your bank, you’re trusting that bank to accurately record that the money left your account and arrived in theirs. The bank is the middleman—and for that service, they charge fees, impose delays, and hold enormous control over your financial life. International transfers can take days and cost significant fees because multiple intermediary banks are involved in verifying and processing the transaction.

This model has worked for decades, but it’s slow, expensive, and requires you to trust institutions that don’t always earn that trust.

How Blockchain Cuts Out the Middleman

Blockchain replaces the middleman with math. Instead of one trusted institution verifying a transaction, thousands of computers on the network verify it simultaneously using cryptographic rules. No single party controls the outcome. The transaction either meets the criteria or it doesn’t—and once confirmed, it’s permanently recorded for anyone on the network to audit.

This is why blockchain is described as trustless—not because it’s untrustworthy, but because trust in a single authority is no longer required.

Traditional Systems vs Blockchain

Traditional Database Problem: One organization controls all data; single point of failure; requires trust in central authority

Traditional Banking Problem: Slow transfers (3-5 days); high fees ($15-$50); multiple intermediaries required

Blockchain Solution: Distributed across thousands of computers; no single point of failure; math-based verification replaces trusted middlemen; transactions settle in minutes for fraction of the cost

How Blockchain Actually Works

Understanding the mechanics makes everything else click into place. It doesn’t require a computer science degree—just a clear walkthrough.

When a new transaction happens on a blockchain network, it gets broadcast to a network of computers called nodes. These nodes collect pending transactions and compete—or cooperate, depending on the system—to verify them and bundle them into a new block. Once verified, that block is added to the chain and the record becomes permanent.

The whole process for Bitcoin takes roughly 10 minutes per block. Newer blockchain systems like Solana can process transactions in under a second, showing just how much the technology has evolved since its debut in 2009.

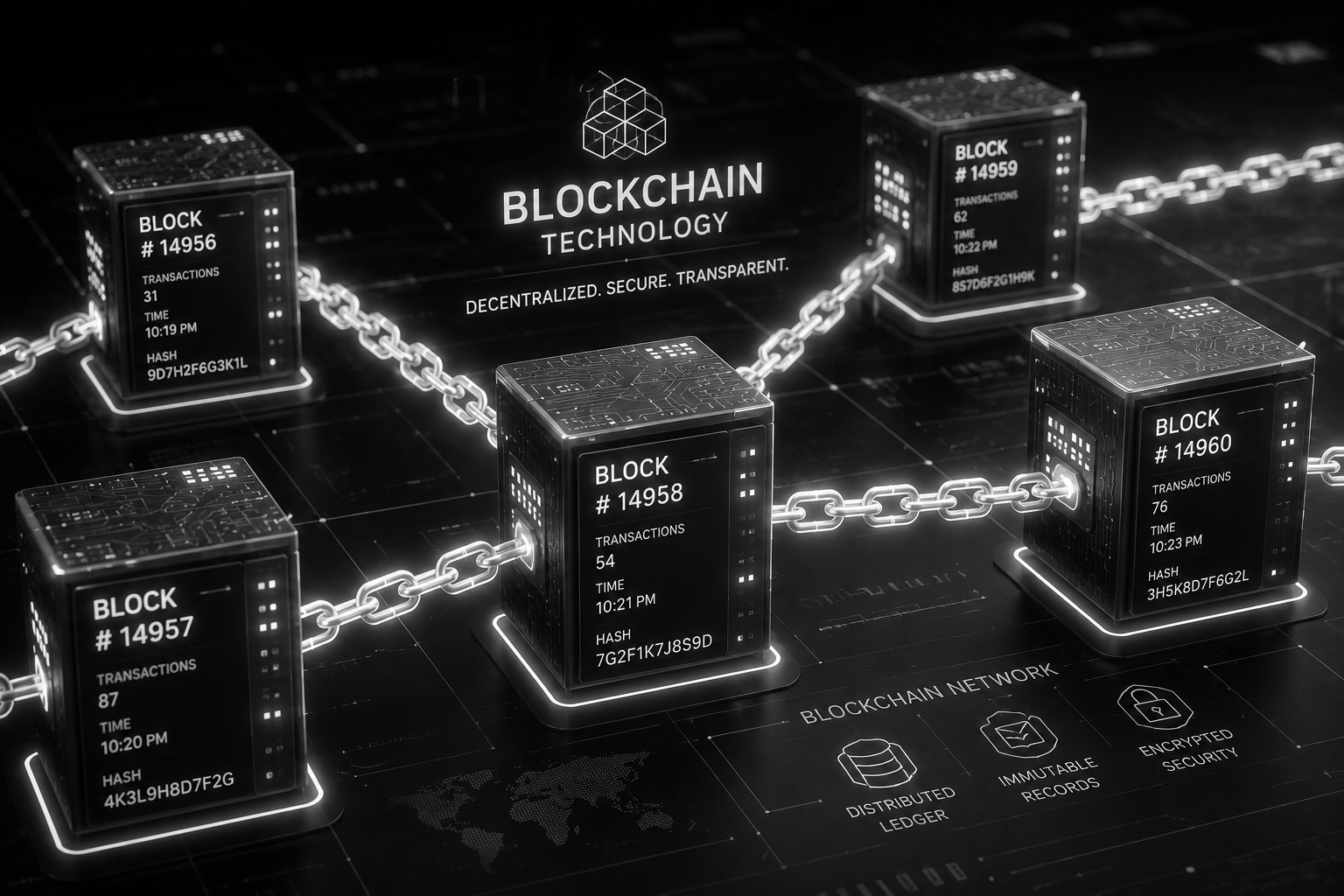

What a “Block” Really Is

Anatomy of a Single Block:

📄 Data — The transaction details (who sent what, to whom, and when)

# Hash — A unique fingerprint code generated for this specific block

← Previous Hash — The fingerprint of the block before it, creating the “chain”

🕐 Timestamp — Exact time the block was created and confirmed

🔒 Nonce — A number used in the verification process (used in proof-of-work systems)

The hash is the most important piece. It’s like a fingerprint—completely unique to the data inside that block. Change even one character of the data, and the hash changes entirely. That’s what makes tampering so easy to detect.

Each block contains the hash of the previous block, which is how they form a chain. If someone tried to alter a transaction three blocks back, the hash would change, which would break the link to the next block, which would break the link to the one after that—invalidating the entire chain from that point forward.

This cascading effect is the core of blockchain security, and it’s elegant in its simplicity.

How Blocks Chain Together

Every new block references the one before it through that embedded hash. Picture a row of combination locks where each lock’s combination is the serial number of the previous lock. To change any one lock, you’d have to re-do every single lock that came after it—across thousands of computers simultaneously. That’s computationally impossible under any realistic scenario, making it a secure foundation for DeFi systems.

This is why blockchain records are described as immutable—once written, they cannot be practically altered without the entire network detecting it.

What “Decentralized” Means in Plain English

Decentralization means no single computer, company, or government controls the blockchain. Instead, an identical copy of the entire blockchain is stored on thousands of nodes (computers) around the world. When a new block is added, every copy updates simultaneously.

If one node goes offline, gets hacked, or tries to submit fraudulent data, the other thousands of nodes reject it. The system doesn’t have a headquarters to attack or a CEO to bribe. That’s a fundamentally different kind of security than anything we’ve built before.

How Transactions Get Verified Without a Bank

Verification happens through a consensus mechanism—a set of rules all nodes agree to follow. Bitcoin uses Proof of Work, where computers race to solve complex math puzzles to earn the right to add the next block. Ethereum switched to Proof of Stake in 2022, where validators are chosen based on how much cryptocurrency they’ve committed as collateral. Both systems achieve the same goal: confirming that a transaction is legitimate without needing a central authority to sign off on it.

The Pros of Blockchain Technology

Blockchain isn’t getting this much attention from banks, governments, and tech giants for no reason. The advantages it offers over traditional systems are real, measurable, and in some cases, genuinely revolutionary. For instance, the comparison between DeFi and traditional finance highlights how blockchain technology can offer greater ownership and control to individuals.

That said, understanding why these benefits exist—not just that they exist—is what separates someone who actually understands blockchain from someone who’s just repeating buzzwords.

| Benefit | What It Means in Practice |

|---|---|

| Decentralization | No single company or government controls the data |

| Immutability | Records cannot be altered once confirmed |

| Transparency | All transactions are publicly auditable |

| Security | Cryptographic hashing makes tampering detectable |

| Lower Fees | Removes costly intermediaries from transactions |

| Financial Inclusion | Accessible to anyone with an internet connection |

1. No Single Point of Failure

Because thousands of nodes each hold a complete copy of the blockchain, there is no central server to take down. A traditional bank’s database going offline means transactions stop. A blockchain network losing hundreds of nodes simultaneously keeps running without interruption—the remaining nodes carry the full record and the system continues functioning. This resilience is especially critical for financial infrastructure where downtime has real-world consequences.

2. Transactions Are Extremely Hard to Hack

To successfully alter data on a blockchain like Bitcoin’s, an attacker would need to control more than 50% of the entire network’s computing power simultaneously—known as a 51% attack. On a large, established blockchain, this is so computationally expensive it becomes economically irrational. The cost of the attack would far exceed any potential gain. This is a fundamentally different security model than a traditional database, where a single successful breach can expose everything.

3. No Third-Party Fees

Sending money internationally through a traditional bank can cost anywhere from $15 to $50 per transfer, plus exchange rate markups, and it can take three to five business days to arrive. A blockchain-based transfer can settle in minutes—sometimes seconds—for a fraction of the cost, with no bank required to approve or process it.

For the roughly 1.4 billion adults worldwide who remain unbanked according to the World Bank, this isn’t just convenient—it’s transformative. Peer-to-peer value transfer without a bank account is now a real possibility for the first time in history.

4. Transparent Yet Private

Every transaction on a public blockchain is visible to anyone—but the identities behind those transactions are represented only by cryptographic wallet addresses, not names or personal information. This creates a system that is simultaneously auditable and pseudonymous. Regulators can track the flow of funds for compliance purposes, while individual users retain meaningful privacy. It’s a balance traditional financial systems have never managed to strike cleanly.

5. Financial Access for the Unbanked

All you need to access a blockchain network is a smartphone and an internet connection. No credit history, no minimum deposit, no government-issued ID required by the network itself. In regions where banking infrastructure is absent or corrupt, blockchain offers a direct on-ramp to financial services—savings, transfers, and even lending—that were previously out of reach for billions of people.

The Cons of Blockchain Technology

Blockchain has genuine weaknesses, and anyone telling you otherwise is selling something. Understanding these limitations is just as important as understanding the benefits—especially if you’re considering using or investing in blockchain-based systems.

The technology is still maturing, and several of these drawbacks are actively being worked on. But right now, in its current state, these are real friction points that matter.

1. It Is Slow Compared to Traditional Databases

Visa’s payment network processes around 24,000 transactions per second. Bitcoin’s blockchain handles approximately 7 transactions per second. Even Ethereum, after its major 2022 upgrade to Proof of Stake, processes roughly 15 to 30 transactions per second under normal conditions. The verification process that makes blockchain secure is also what makes it slow—every node must reach consensus before a block is finalized, and that takes time. For global-scale financial infrastructure, this gap is still a serious obstacle.

Transaction Speed Reality Check

Visa: ~24,000 transactions per second

Ethereum: 15-30 transactions per second

Bitcoin: ~7 transactions per second

Bitcoin Block Time: ~10 minutes per block

2. Energy Consumption Is a Real Problem

Bitcoin’s Proof of Work consensus mechanism requires enormous amounts of computing power—and therefore electricity. At its peak, the Bitcoin network consumed more electricity annually than some mid-sized countries, according to data from the Cambridge Centre for Alternative Finance. This is a legitimate environmental concern, not just a talking point.

Proof of Stake blockchains like Ethereum have dramatically reduced their energy footprint—Ethereum’s merge to Proof of Stake in September 2022 cut its energy consumption by approximately 99.95%. But Bitcoin, the largest blockchain by market cap, still relies on Proof of Work, and that isn’t changing anytime soon.

3. It Has Been Used for Illegal Activity

The pseudonymous nature of blockchain transactions has made it attractive for illicit use—ransomware payments, darknet marketplace transactions, and money laundering have all involved cryptocurrency at various points. While blockchain’s transparency actually makes it easier for law enforcement to trace funds compared to cash, the perception problem is real and has contributed to regulatory pushback in multiple countries. It’s a genuine downside that deserves honest acknowledgment.

4. Regulation Is Still a Grey Area

Blockchain operates across borders, but laws don’t. Different countries have wildly different stances—El Salvador made Bitcoin legal tender in 2021, while China banned cryptocurrency transactions entirely. This regulatory patchwork creates uncertainty for businesses building on blockchain infrastructure and for individuals trying to use it compliantly.

Until clearer international frameworks emerge, this uncertainty acts as a brake on mainstream adoption. Businesses are hesitant to fully commit to technology whose legal status could shift dramatically with a single piece of legislation.

The Four Real Drawbacks

1. Speed: Bitcoin processes ~7 TPS vs Visa’s 24,000 TPS

2. Energy: Bitcoin’s Proof of Work consumes massive electricity; Ethereum’s 2022 switch to Proof of Stake cut energy use 99.95%

3. Illegal Use: Ransomware, darknet markets; $3.8B stolen from crypto platforms in 2022

4. Regulation: El Salvador legalized Bitcoin; China banned crypto; international frameworks still emerging

Where Blockchain Is Used Today

Blockchain has moved well beyond theoretical whitepapers and cryptocurrency speculation. Right now, across multiple industries, it is solving real operational problems that traditional systems have struggled with for decades.

Cryptocurrency Transactions

This is where it all started, and cryptocurrency remains the most widely used application of blockchain technology today. Bitcoin processes billions of dollars in transactions daily as a store of value and peer-to-peer payment system. Stablecoins like USDC and USDT—which are pegged to the US dollar and run on blockchain networks—are being used for remittances, international trade settlements, and as inflation hedges in countries with unstable local currencies.

The cryptocurrency use case has also served as the testing ground for every major blockchain innovation—smart contracts, layer-2 scaling solutions, and decentralized finance (DeFi) protocols all emerged from the crypto ecosystem and are now being adapted for broader enterprise use.

Supply Chain Tracking

Every year, counterfeit goods, food contamination outbreaks, and shipping fraud cost global businesses hundreds of billions of dollars—and most of it happens because supply chains rely on fragmented, paper-based, or siloed record systems that nobody fully trusts. Blockchain fixes this by creating a single shared record that every participant in the supply chain—manufacturers, shippers, retailers, and regulators—can access and verify in real time.

Walmart has been using a blockchain-based food traceability system built on IBM Food Trust since 2019. Before blockchain, tracing the origin of contaminated leafy greens took about seven days. With blockchain, the same trace takes approximately 2.2 seconds. That speed difference is the gap between a manageable recall and a public health crisis.

Beyond food, companies like Maersk—the world’s largest shipping company—have used blockchain to digitize and share shipping documents across international supply chains, cutting paperwork processing times dramatically and reducing the risk of document fraud. The use case here isn’t theoretical. It’s already running at industrial scale.

Walmart’s Blockchain Success Story

Before Blockchain: 7 days to trace contaminated food source

After Blockchain: 2.2 seconds to trace contaminated food source

That speed difference is the gap between a manageable recall and a public health crisis

Healthcare Record Management

Medical records are fragmented across hospitals, clinics, and specialists—and that fragmentation costs lives. A patient arriving unconscious at an emergency room in a different city may have no accessible medical history. Blockchain offers a model where patient records are stored securely on a distributed ledger, accessible only with the patient’s cryptographic key, but available instantly to any authorized provider anywhere in the world. The MedRec project, developed by researchers at MIT, demonstrated this concept using Ethereum, allowing patients to control exactly who could access their records and creating a permanent, auditable log of every access event.

Bitcoin vs. Blockchain: They Are Not the Same Thing

This is one of the most common points of confusion for beginners, and it matters because conflating them leads to misunderstanding both. Bitcoin is a cryptocurrency—a digital form of money. Blockchain is the underlying technology that Bitcoin runs on. Saying Bitcoin and blockchain are the same thing is like saying the internet and Gmail are the same thing. One is the infrastructure; the other is an application built on it.

Bitcoin was the first real-world implementation of blockchain technology, introduced in Satoshi Nakamoto’s 2008 whitepaper. But in the years since, thousands of other blockchains have been built—Ethereum, Solana, Cardano, Polkadot—each with different rules, speeds, and use cases. Many of these have nothing to do with digital currency at all. Ethereum’s blockchain, for example, is primarily used to run smart contracts and decentralized applications.

Bitcoin vs. Blockchain — Side by Side

| Bitcoin | Blockchain |

|---|---|

| A specific cryptocurrency | A type of database technology |

| One application of blockchain | The infrastructure Bitcoin runs on |

| Used primarily as digital money | Used across finance, healthcare, logistics, and more |

| Created in 2009 | Concept formalized in Bitcoin’s 2008 whitepaper |

| Controlled by no single entity | Can be public, private, or hybrid |

The practical takeaway is this: blockchain technology will continue to exist and expand regardless of what happens to Bitcoin’s price. They are related, but they are not the same investment, the same technology, or the same conversation.

Is Blockchain the Future or Just Hype?

The honest answer is both—and knowing which parts are which is what matters. Blockchain solves real problems in specific contexts, but it has also attracted enormous speculation, inflated promises, and outright fraud. Separating the signal from the noise requires looking at where it’s actually delivering results versus where it’s being used as a marketing buzzword.

Where the Technology Is Headed

- Central Bank Digital Currencies (CBDCs): Over 130 countries are actively exploring or piloting government-issued digital currencies built on blockchain infrastructure, according to the Atlantic Council’s CBDC tracker.

- Tokenization of Real-World Assets: Everything from real estate to fine art is being tokenized on blockchain networks, allowing fractional ownership and dramatically lowering the barrier to investment.

- Decentralized Identity: Blockchain-based digital IDs could allow individuals to verify their identity online without surrendering personal data to centralized platforms.

- Smart Contract Automation: Legal agreements, insurance payouts, and financial derivatives are increasingly being executed automatically by smart contracts—reducing processing time from days to seconds.

- Interoperability Protocols: Projects like Polkadot and Cosmos are building systems that allow different blockchains to communicate with each other, solving the fragmentation problem that has limited large-scale adoption.

The most important developments aren’t happening in cryptocurrency price speculation—they’re happening in enterprise infrastructure, government pilots, and protocol-level engineering. The technology is genuinely maturing.

Layer-2 scaling solutions like the Lightning Network for Bitcoin and Optimism for Ethereum are already processing transactions faster and cheaper by handling them off the main chain and settling periodically. This directly addresses the speed and cost limitations that have held blockchain back from competing with systems like Visa at scale.

The next five years will likely determine whether blockchain becomes foundational global infrastructure or remains a niche technology used primarily in finance and logistics. The trajectory is positive, but it is not guaranteed—and it depends heavily on regulatory clarity and the industry’s ability to solve remaining technical limitations.

Where Blockchain Is Actually Headed

CBDCs: 130+ countries exploring government digital currencies

Asset Tokenization: Real estate, art fractionally owned on blockchain

Decentralized Identity: Verify identity without surrendering personal data

Smart Contracts: Legal agreements execute automatically in seconds

Interoperability: Different blockchains communicating with each other

What Needs to Change for Mass Adoption

Three things need to happen for blockchain to reach true mainstream adoption. First, user experience needs to become dramatically simpler. Right now, managing a crypto wallet, understanding gas fees, and avoiding irreversible transaction errors requires a level of technical literacy that most people don’t have and shouldn’t need. The technology needs to become invisible—the way most people use the internet without understanding TCP/IP protocols.

Second, regulatory clarity needs to arrive. Businesses cannot confidently build on blockchain infrastructure when the legal ground beneath them can shift overnight. Clear, consistent international frameworks—particularly around digital assets, smart contract enforceability, and data privacy—are a prerequisite for institutional-scale adoption. The technology is ready; the legal infrastructure is lagging significantly behind.

Three Requirements for Mass Adoption

1. Simpler User Experience

Technology must become invisible—no more managing wallets, gas fees, irreversible errors

2. Regulatory Clarity

Clear international frameworks for digital assets, smart contracts, data privacy

3. Proven Enterprise Success

More real-world results like Walmart’s 7-day → 2.2-second traceability improvement

Frequently Asked Questions

These are the questions beginners ask most often—answered directly, without unnecessary complexity.

Is Blockchain the Same as Cryptocurrency?

No. Blockchain is the technology; cryptocurrency is one application built on top of it. Think of blockchain as the road and cryptocurrency as one type of vehicle that drives on it. Many other vehicles—supply chain systems, medical records, digital contracts—can use the same road.

You can interact with blockchain technology, benefit from it, or even build on it without ever owning or transacting in cryptocurrency. The two are connected by history and by Bitcoin’s origin story, but they are fundamentally separate things.

Can Blockchain Be Hacked?

The blockchain itself—the core chain of verified blocks—is extraordinarily difficult to attack on a large, established network. A successful attack would require controlling more than 50% of the network’s computing power simultaneously, which on Bitcoin’s network would cost billions of dollars and would likely be detected and countered before completion.

However, the surrounding ecosystem is absolutely vulnerable. Cryptocurrency exchanges, digital wallets, smart contract code, and individual user accounts have all been successfully hacked. In 2022 alone, over $3.8 billion was stolen from crypto-related platforms according to Chainalysis—almost none of it by attacking the blockchain itself, but by exploiting the software and human error built around it. The chain is secure; the ecosystem around it is not always.

Do You Need to Own Crypto to Use Blockchain?

No. Many blockchain applications function without any direct cryptocurrency involvement from the end user. Walmart’s food traceability system, IBM’s TradeLens shipping platform, and various government land registry pilots all use blockchain as a back-end record-keeping system—consumers and users interact with them without ever touching a cryptocurrency.

Where transaction fees are involved—such as using Ethereum’s network to run a smart contract—some cryptocurrency is typically required to pay those fees. But this is increasingly being abstracted away by applications that handle it on the backend, the same way most people don’t manually pay for the server costs of the websites they use.

The short answer: for most consumer-facing blockchain applications being built today, the goal is specifically to make cryptocurrency invisible to the end user—similar to how you don’t need to understand payment rail infrastructure to tap your credit card.

Do You Need Crypto? It Depends on the Use Case

| Use Case | Crypto Required? |

|---|---|

| Sending Bitcoin to someone | Yes |

| Using a DeFi lending platform | Yes |

| Tracking a food shipment via IBM Food Trust | No |

| Verifying a digital diploma on a blockchain | No |

| Using a blockchain-based healthcare record system | No |

Is Blockchain Technology Legal?

In most countries, yes—blockchain technology itself is legal. The legal questions primarily arise around specific applications, particularly cryptocurrency transactions, which are regulated differently depending on jurisdiction. The United States, European Union, United Kingdom, and most developed economies permit blockchain use and are actively developing regulatory frameworks to govern it more precisely.

A small number of countries—most notably China—have imposed bans on cryptocurrency transactions, though even China continues to develop its own state-controlled blockchain infrastructure for its digital yuan (e-CNY). The technology is not what’s being restricted; it’s specific financial applications of it that face regulatory scrutiny. Always check your local regulations if you’re considering using blockchain for financial purposes. For a deeper understanding of how blockchain technology compares, you might find this blockchain comparison between Ethereum and Solana insightful.

How Is Blockchain Different from a Regular Database?

A regular database is like a spreadsheet controlled by one organization—they can read it, edit it, delete rows, and restrict who sees it. Blockchain is more like a spreadsheet that’s simultaneously stored on thousands of computers, where every entry is permanent, every change is visible to all participants, and no single party controls it.

Traditional databases are faster and more flexible—they’re ideal when you need one trusted party to manage data efficiently. Blockchain is slower but far more trustworthy in environments where multiple parties need to share data without trusting a central administrator.

The key technical differences come down to structure, control, and mutability. Traditional databases use editable tables; blockchain uses append-only linked blocks. Traditional databases have administrators who can modify records; blockchain requires network-wide consensus to add anything. Traditional databases are efficient; blockchain is resilient.

Neither technology is universally superior—they solve different problems. A hospital managing internal patient records might use a traditional database for speed and control. A consortium of hospitals sharing records across organizations might use blockchain to ensure no single institution can tamper with the shared data. The right tool depends entirely on the problem being solved.

If data integrity, multi-party trust, and tamper resistance are the priority—blockchain wins. If speed, flexibility, and cost efficiency are the priority for a single trusted organization—a traditional database is the better choice. Understanding that distinction is what separates informed blockchain thinking from hype.

Blockchain technology is revolutionizing the way we think about data security and transparency. It offers a decentralized and tamper-proof way to record transactions, making it a cornerstone of the cryptocurrency world. For those interested in how blockchain interacts with traditional finance, this beginner guide to DeFi vs traditional finance provides valuable insights into the differences in ownership and control.

Blockchain vs Traditional Database

Traditional Database: One organization controls; fast and flexible; editable records; administrators can modify data

Blockchain: Thousands of computers store copies; slower but trustworthy; permanent records; requires network consensus to add anything

The Right Choice: Traditional database when speed and single-party control needed; blockchain when data integrity and multi-party trust are priority

Do Your Own Research (DYOR): This article is for educational purposes only and does not constitute financial, investment, or legal advice. Blockchain technology and cryptocurrency investments carry significant risks. Always conduct thorough research and consult with qualified professionals before making any financial decisions related to blockchain or cryptocurrency.

Latest

Blockchain

08 Jul 2026

Blockchain

04 Jul 2026

Blockchain

21 May 2026

Blockchain

13 May 2026

Blockchain

15 Mar 2026