Coinposters

Best Crypto Wallets for Businesses: Open Source, Insured & Regulated Solutions

The best crypto wallets for businesses in 2026 combine self-custody, multi-user access with role-based permissions, and compliance-ready reporting, no single feature is enough on its own, and the right choice depends entirely on whether you need treasury storage, payment processing, or DeFi access.

Article at a Glance

- Most businesses using personal crypto wallets are exposing company funds to unnecessary risk, the gap between consumer and business-grade wallet features is wider than most CFOs realize.

- The best crypto wallets for businesses in 2026 combine self-custody, multi-user access with role-based permissions, and compliance-ready reporting, no single feature alone is enough.

- Tangem’s hardware wallet uses EAL6+ certified chips and eliminates seed phrase risk entirely, a critical advantage for teams managing shared treasury funds.

- Regulated and insured wallets serve different purposes, regulated wallets simplify compliance, while insurance protects against specific loss events, and having one does not mean you have the other.

- The right wallet depends entirely on your use case: treasury storage, payment processing, and DeFi access all require different tools.

Table of Contents

- Most Businesses Are Using the Wrong Crypto Wallet

- What Makes a Crypto Wallet Genuinely Business-Grade

- Open Source Crypto Wallets for Businesses

- 1. Tangem Business Wallet

- 2. MetaMask Institutional

- 3. Ledger Enterprise

- 4. CoinsPaid Business Wallet

- 5. Coinbase Prime

- Insured Crypto Wallets: What Coverage Actually Means

- Regulated Crypto Wallets: Compliance Without Complexity

- Side-by-Side Comparison: Top 5 Business Crypto Wallets

- How to Choose the Right Wallet for Your Business

- Tangem Is the Strongest All-Around Business Wallet

- Frequently Asked Questions

If your business is storing or transacting crypto using a wallet built for individual users, you already have a security problem, you just might not know it yet. This guide to the best crypto wallets for businesses breaks down exactly why, and what to do instead.

Tangem, a leader in hardware crypto wallet solutions, provides this breakdown to help businesses move past consumer-grade tools and into purpose-built infrastructure that can actually support treasury management, team access, and compliance at scale. The difference between a personal wallet and a business wallet isn’t cosmetic, it’s architectural.

Most Businesses Are Using the Wrong Crypto Wallet

The majority of small and mid-sized businesses that hold crypto started with whatever wallet their founder or finance lead already had. That usually means MetaMask, Trust Wallet, or a hardware device with a single recovery seed, all tools designed with one user in mind.

Personal Wallets vs. Business Wallets: A Critical Difference

A personal wallet is built around one private key, controlled by one person. That’s fine for an individual, but it creates a single point of failure the moment a second employee needs access. Business wallets are built differently, they’re designed to distribute control, enforce approval rules, and keep a verifiable record of every transaction that moves through the account.

The core distinction comes down to governance. Personal wallets have none. Business wallets are built around it.

When a CFO or treasury manager holds the only seed phrase and then leaves the company, business funds can become permanently inaccessible. When a single employee with full wallet access gets phished, the entire treasury is at risk. These aren’t edge cases, they’re documented, recurring losses that happen specifically because businesses use tools that weren’t built for them.

“The difference between a personal wallet and a business wallet isn’t cosmetic, it’s architectural.”

What Happens When a Business Uses a Consumer Wallet

The failure modes are specific and severe. There’s no audit trail when someone initiates a transfer. There’s no approval gate that requires a second signatory. There’s no role-based permission system that limits what a junior employee can do versus a finance director. The wallet treats every user with access as having total, unrestricted control, which is exactly how unauthorized transfers and internal theft happen. For businesses, understanding the differences between hot wallets and cold wallets can be crucial in preventing such risks.

Why 2026 Demands a Higher Standard

Regulatory pressure on crypto-holding businesses has intensified significantly. Tax authorities in the US, EU, and across Asia-Pacific now require detailed transaction records, and businesses that can’t produce them face real penalties. At the same time, the average value of business crypto treasuries has grown, making them more attractive targets. The tools businesses use need to match the environment they’re operating in.

What Makes a Crypto Wallet Genuinely Business-Grade

Business-grade doesn’t mean expensive or complicated. It means the wallet was designed to handle the specific problems that arise when more than one person needs access to shared funds, and when those funds need to move in ways that can be documented and defended to auditors.

There are four features that separate a real business wallet from a consumer wallet with a company logo on it.

Multi-User Access and Role-Based Permissions

A proper business wallet lets you assign different levels of access to different team members. A bookkeeper might be able to view balances and export transaction data. A finance manager might be able to initiate transfers up to a set limit. Only an authorized director can approve large outgoing payments. This kind of tiered access isn’t a luxury, it’s a basic internal control that any serious finance operation requires. For those considering the security of their digital assets, understanding the differences between a hot wallet and a cold wallet is crucial.

Approval Workflows That Prevent Unauthorized Transfers

Multi-signature (multisig) transaction approval means that no single person can move funds unilaterally. A 2-of-3 multisig setup, for example, requires any two of three designated signers to approve a transaction before it executes. This eliminates the single-point-of-failure problem and makes internal fraud significantly harder to execute without detection.

Audit Trails and Compliance-Ready Reporting

Every transaction your business makes in crypto needs to be documented, who initiated it, when, how much, to which address, and for what purpose. Business wallets that generate structured, exportable transaction histories make tax filing and regulatory audits manageable. Those that don’t leave your finance team doing manual reconciliation from blockchain explorers, which is time-consuming and error-prone.

Self-Custody vs. Custodial: Which Is Safer for Business Funds

Custodial wallets, where a third party holds your private keys, introduce counterparty risk. If that provider is hacked, goes insolvent, or freezes withdrawals, your funds are inaccessible. Self-custody wallets give your business direct control over its private keys, eliminating that dependency. For businesses managing meaningful treasury balances, self-custody with proper internal controls is the stronger position, and it’s the architecture that the best business wallets on this list are built around.

Open Source Crypto Wallets for Businesses

Open source means the wallet’s code is publicly available and can be independently reviewed by anyone, security researchers, developers, and auditors included. For a business making a security decision about where to store company funds, this is a meaningful distinction. Understanding the difference between a hot wallet and a cold wallet can also be crucial for businesses focused on security.

Closed source wallets ask you to trust the vendor’s claims about their security architecture. Open source wallets let the broader technical community verify those claims independently. When vulnerabilities are found in open source code, they tend to get identified and patched faster because more eyes are on the codebase.

Why Open Source Matters for Corporate Security

When a security researcher finds a critical vulnerability in an open source wallet, the fix is typically public, verifiable, and deployed quickly. The entire process is transparent. For businesses operating under compliance frameworks that require documented security practices, using a wallet with a publicly audited codebase is a defensible position. It means your security isn’t resting on a vendor’s word alone.

The Risks of Closed-Source Wallets for Business Treasury

Closed-source wallets aren’t automatically insecure, but they do require a level of trust in the vendor that businesses should think carefully about. You can’t verify what the code is doing with your private keys. You can’t confirm that encryption is implemented as described. And if the company behind the wallet is acquired, pivots, or shuts down, your ability to audit or migrate becomes dependent on their cooperation. For more on securing your crypto assets, consider understanding the differences between hot and cold wallets.

For small transaction volumes or payments processing, this tradeoff may be acceptable. For treasury management, where significant company funds sit long-term, the inability to independently verify security architecture is a real risk that businesses should weigh deliberately.

1. Tangem Business Wallet

Tangem is a hardware wallet built around NFC-enabled smart cards, each containing a secure chip certified to EAL6+, the same security standard used in biometric passports and high-security government credentials. What makes Tangem genuinely different for business use is what it removes from the security equation: the seed phrase.

Every other hardware wallet generates a 12 or 24-word seed phrase that must be stored securely. That seed phrase is a single point of failure, if it’s lost, stolen, photographed, or written down somewhere accessible, full wallet access can be compromised. Tangem eliminates the seed phrase entirely. The private key is generated and stored on the card itself and never leaves it, making it impossible to leak through human error. For those considering other crypto investments, it’s worth exploring the fastest growing altcoins in 2026.

Hardware-Based Security Without a Seed Phrase

The private key on a Tangem card is generated inside the EAL6+ certified chip during setup and cannot be extracted, not by the user, not by Tangem, and not by an attacker with physical access to the card. Transactions are signed on the card itself, and the key never touches the connected device. For businesses where multiple people might handle setup or onboarding, removing the seed phrase from the process eliminates an entire category of operational security risk.

Multi-Card Backup System and Team Access

Tangem’s business setup uses a multi-card architecture. A wallet can be configured with two or three cards that share access to the same funds. Each card independently controls the wallet, which means backup and team access are handled at the hardware level, not through a shared password or a copied seed phrase stored in a spreadsheet somewhere. For those interested in exploring more about cryptocurrency investments, you might find the insights on Dogecoin as a good investment helpful.

How Tangem Multi-Card Business Access Works

Card 1 (Primary): Held by the business owner or CFO for day-to-day access and transaction signing.

Card 2 (Backup/Secondary Approver): Held by a second authorized team member or stored securely offsite as a backup.

Card 3 (Optional Third Backup): Provides redundancy for larger teams or higher-security treasury setups.

Each card operates independently. If one card is lost or damaged, the others maintain full wallet access, no seed phrase recovery required.

This architecture directly addresses the single-point-of-failure problem that makes consumer wallets dangerous for business use. The multi-card setup can be distributed across key personnel so no one person holds exclusive control over company funds. For businesses considering long-term investments, this setup offers enhanced security and peace of mind.

For businesses with structured finance teams, this is a hardware-native answer to the governance problem, no third-party multisig service required, no complex smart contract configuration, just physical card distribution that maps directly to your organizational access controls.

90+ Blockchain Support and Stablecoin Yield Features

Tangem supports over 90 blockchain networks, including Bitcoin, Ethereum, Solana, BNB Chain, Polygon, Avalanche, Tron, and all major EVM-compatible chains. For businesses that operate across multiple chains, receiving payments in USDC on Ethereum, holding BTC in treasury, and interacting with DeFi protocols on Solana, a single Tangem setup covers the full stack. The wallet also integrates stablecoin yield features, allowing businesses to put idle treasury assets to work without moving funds off the hardware device.

Best For: Teams That Need Self-Custody With Zero Seed Phrase Risk

Tangem is the strongest fit for businesses that want hardware-level security without the operational complexity of seed phrase management. That includes Web3 companies, crypto-native startups, iGaming operators, and any business where multiple team members need wallet access but where a single compromised seed phrase could be catastrophic.

It’s also a compelling choice for businesses that are new to crypto treasury management and want a setup that’s genuinely difficult to misconfigure. The absence of a seed phrase doesn’t reduce security, it removes the most common vector through which business crypto funds are lost.

2. MetaMask Institutional

MetaMask Institutional (MMI) is the enterprise version of the world’s most widely used Web3 wallet, rebuilt specifically for funds, DAOs, and businesses that need to operate on-chain at scale. Where the consumer version of MetaMask is a browser extension with no governance features, MMI adds a full layer of institutional controls on top of the same Web3 connectivity that makes MetaMask the default interface for decentralized applications.

Web3 Integration and DeFi Access for Businesses

MMI connects directly to thousands of decentralized applications across Ethereum and EVM-compatible chains, giving businesses native access to DeFi protocols, NFT platforms, and on-chain governance systems without routing transactions through a custodian. For Web3-native businesses, DAOs, DeFi funds, blockchain gaming companies, and crypto-native fintech, this direct on-chain access is the primary reason to choose MMI over a more traditional institutional wallet.

MetaMask Institutional: Key Business Features at a Glance

Custodian Integrations: Connects to Fireblocks, Qredo, Cactus Custody, and other institutional custodians for key management.

Transaction Approval Workflows: Multi-party approval rules configurable per wallet or per transaction type.

DeFi Access: Direct connection to Uniswap, Aave, Compound, Curve, and thousands of other protocols.

Reporting: Exportable transaction history with institutional-grade audit trails.

Chain Support: Ethereum mainnet plus all major EVM-compatible networks including Polygon, Arbitrum, Optimism, and BNB Chain.

The custodian integration model is what makes MMI genuinely institutional. Rather than managing private keys directly within the wallet interface, MMI connects to your existing custody provider, so your keys stay in a Fireblocks MPC vault or a Qredo network while your team interacts with DeFi through the familiar MetaMask interface. This means you don’t have to choose between DeFi access and institutional key security.

For businesses already using an institutional custodian, this is a significant advantage. The learning curve for your team is minimal because the interface is identical to the MetaMask they may already know, but the security architecture underneath is enterprise-grade.

Governance and Reporting Tools for Compliance Teams

MMI includes configurable transaction approval workflows that can require multiple signers before a transaction executes. These workflows can be set at the wallet level or the transaction level, meaning you can require a single approver for routine DeFi interactions but three approvers for any transfer above a defined threshold. That kind of granular rule-setting maps directly to how finance teams manage spending controls in traditional corporate environments.

The reporting layer exports structured transaction data that finance and compliance teams can use for tax reporting, internal audit, and regulatory submissions. For businesses operating under MiCA in the EU or reporting under FASB’s updated crypto accounting standards, having clean, structured on-chain data in an exportable format is no longer optional, it’s a filing requirement.

Best For: Web3-Native Businesses and DeFi Operators

MetaMask Institutional is the right tool for businesses whose core operations happen on-chain, DAOs managing protocol treasuries, crypto funds executing DeFi strategies, Web3 gaming companies handling in-game asset flows, and fintech businesses building on Ethereum infrastructure. If your business needs deep DeFi access combined with institutional governance, MMI is the most purpose-built option on this list for that specific use case.

3. Ledger Enterprise

Ledger Enterprise is the institutional arm of Ledger, the company behind the world’s best-selling hardware wallets. Where consumer Ledger devices are single-user cold storage tools, Ledger Enterprise is a full platform built for organizations, combining cold storage security with multi-user governance, policy engines, and a broad integration ecosystem designed for corporate treasury operations.

Ledger Enterprise Security Architecture Summary

Device Security: Proprietary BOLOS operating system running on CC EAL5+ certified secure element chips.

Key Management: Private keys generated and stored on hardware devices, never exposed to connected systems.

Governance Layer: Configurable approval policies with multi-operator transaction signing requirements.

Connectivity: API integrations with exchanges, OTC desks, DeFi protocols, and prime brokers.

Asset Support: 5,000+ cryptocurrencies and tokens across major networks.

The platform separates key management from transaction initiation, meaning the people who can request a transfer are not necessarily the same people who approve and sign it. This separation of duties is a foundational internal control in traditional finance, Ledger Enterprise brings it natively to crypto treasury management.

Ledger Enterprise also offers a Software-as-a-Service deployment model, which means businesses don’t need to build and maintain their own key management infrastructure. The platform handles hardware provisioning, firmware updates, and security monitoring, reducing the operational overhead of running a cold storage treasury at scale.

Cold Storage Architecture and Vault Security

Every transaction signed through Ledger Enterprise is signed on a hardware device, not in software, not in a browser, and not on a cloud server. The private keys exist only on the physical device. This cold storage architecture means that even if the Ledger Enterprise platform itself were compromised at the software level, an attacker still could not access or move funds without physical access to the signing hardware. For large treasury balances where the cost of a breach would be catastrophic, this hardware-enforced boundary is the strongest protection currently available in the market.

Multi-Signature Transaction Approval

Ledger Enterprise’s policy engine allows businesses to configure transaction approval rules at a granular level. A company can require that any outgoing transfer above $50,000 requires signatures from three of five designated approvers, while routine operational payments below $5,000 require only one. These policies are enforced at the hardware level, they cannot be bypassed by software alone, which means even a compromised admin account cannot unilaterally override the approval requirements.

This is a meaningful security distinction. Software-enforced approval rules can be circumvented by anyone with sufficient access to the underlying system. Hardware-enforced rules cannot, the hardware device itself will refuse to sign a transaction that doesn’t satisfy the configured policy conditions. For those interested in cryptocurrency investments, understanding the differences between Bitcoin and Ethereum is crucial for long-term investment strategies.

Best For: Large Treasuries Requiring Maximum Cold Storage Security

Ledger Enterprise is the right choice for businesses managing significant long-term crypto holdings where security takes absolute priority over operational convenience. That includes publicly traded companies holding Bitcoin on their balance sheet, crypto funds with institutional LP capital, and fintech companies that need to demonstrate to regulators and auditors that their custody architecture meets institutional standards.

4. CoinsPaid Business Wallet

CoinsPaid takes a fundamentally different approach to business crypto infrastructure. Where the other wallets on this list are primarily treasury and custody solutions, CoinsPaid is built around payment processing, specifically, helping businesses accept crypto payments, convert them to fiat, and manage high-volume transaction flows without building their own blockchain infrastructure from scratch.

Merchant Payment Processing and Checkout Integration

CoinsPaid provides a business wallet with an integrated payment gateway that connects directly to e-commerce platforms, point-of-sale systems, and custom checkout flows via API. Businesses can generate unique payment addresses per transaction, display real-time crypto-to-fiat pricing at checkout, and handle payment confirmation without any manual intervention. For an online retailer or service business adding crypto as a payment method, the CoinsPaid setup is significantly more practical than pointing customers at a raw wallet address and reconciling transactions manually.

The platform supports Bitcoin, Ethereum, Litecoin, USDT, USDC, and a range of other cryptocurrencies at checkout, with automatic conversion available so merchants can price in their local fiat currency and receive funds in that currency regardless of what the customer pays in.

Fiat Settlement and Currency Conversion

CoinsPaid’s built-in exchange and settlement layer means businesses don’t need to hold crypto longer than they choose to. Incoming payments can be automatically converted to EUR, USD, or other supported fiat currencies and settled to a linked bank account on a scheduled basis. For businesses that want the revenue benefits of accepting crypto without the volatility exposure of holding it, this automatic settlement flow removes the treasury management complexity entirely.

Best For: E-Commerce and Merchant Businesses Accepting Crypto Payments

CoinsPaid is the strongest fit for businesses whose primary need is accepting crypto as payment rather than managing a crypto treasury. That includes online retailers, subscription service platforms, iGaming operators processing player deposits and withdrawals, and any merchant business that wants to add crypto payment rails without building and managing their own wallet infrastructure.

It’s worth being direct about the tradeoff: CoinsPaid is a custodial platform, which means the business does not hold its own private keys. For payment processing at volume, this is a reasonable tradeoff, the operational simplicity justifies the custody dependency. For businesses that also need to hold significant crypto reserves long-term, CoinsPaid should be paired with a self-custody treasury solution rather than used as the sole wallet.

The platform has processed billions of dollars in crypto transactions, primarily for the iGaming sector, and was previously VASP-licensed in Estonia. Note that Estonia’s legacy VASP regime sunset on July 1, 2026, and businesses like CoinsPaid are in transition to full MiCA CASP authorization under the EU’s new framework, current licensing status should be independently verified before relying on it for compliance purposes. For high-volume merchant use cases, the underlying payment infrastructure is proven at scale in ways that newer or smaller payment processors simply aren’t yet.

5. Coinbase Prime

Coinbase Prime is the institutional product arm of Coinbase, one of the few crypto companies to have successfully navigated US regulatory requirements at scale. It combines custody, trading, financing, and reporting in a single platform built specifically for institutional clients, hedge funds, asset managers, corporate treasuries, and publicly traded companies that need to hold and trade crypto under the same compliance standards as their traditional asset portfolios.

Institutional-Grade Custody and Prime Brokerage

Coinbase Prime uses a segregated cold storage architecture where client assets are held separately from Coinbase’s corporate funds. The custody layer is operated by Coinbase Custody Trust Company, a New York-chartered limited purpose trust company regulated by the New York Department of Financial Services (NYDFS). This regulatory charter means Coinbase Custody operates under the same fiduciary standards as traditional bank custodians, a meaningful distinction for institutional investors whose mandates require regulated custody.

Beyond custody, Coinbase Prime offers prime brokerage services including algorithmic trading, OTC execution, margin financing, and portfolio reporting, all integrated within the same platform. For institutions that need to actively manage a crypto portfolio rather than simply hold assets, the combination of regulated custody and trading infrastructure in a single interface reduces operational complexity significantly.

Regulatory Compliance and Insurance Coverage

Coinbase maintains crime insurance covering digital assets held in its hot wallet systems, and client assets in cold storage are held off-balance-sheet in a bankruptcy-remote structure, meaning that in a Coinbase insolvency scenario, client assets are protected from creditor claims. Coinbase Prime also provides detailed tax reporting, transaction records, and audit support that meet the documentation requirements of US institutional investors, including those subject to SEC reporting obligations.

Best For: Institutional Investors and High-Volume Trading Operations

Coinbase Prime is the right choice for institutions that need regulated custody, active trading capabilities, and the credibility of a publicly listed, NYDFS-regulated custodian. That means hedge funds, family offices, endowments, and corporate treasury teams at publicly traded companies where the regulatory and fiduciary requirements around crypto custody are as demanding as those around traditional asset classes.

It’s not the right fit for businesses that want self-custody or those that prioritize decentralization, Coinbase Prime is explicitly a custodial solution, and the value proposition is entirely built around regulatory compliance and institutional infrastructure rather than key sovereignty. For the businesses it’s designed for, that tradeoff is the point.

Insured Crypto Wallets: What Coverage Actually Means

Crypto wallet insurance is one of the most misunderstood features in the institutional wallet market. Providers advertise insurance coverage as a security differentiator, and it is, but only if you understand precisely what the insurance actually covers, because the gap between what businesses assume is covered and what policies actually protect is significant.

What Crypto Wallet Insurance Covers and What It Does Not

Most crypto custody insurance policies are crime insurance policies, not deposit insurance equivalents. They cover specific, defined loss events, typically third-party theft, physical theft of hardware, and in some cases employee dishonesty. What they generally do not cover includes losses from private key mismanagement by the client, losses resulting from smart contract exploits, market value losses, or losses from phishing attacks where the client voluntarily authorized a fraudulent transaction.

The distinction matters most in the scenarios businesses actually worry about. A sophisticated social engineering attack that tricks an employee into authorizing a fraudulent transfer is unlikely to be covered by a standard crime policy, because from the insurer’s perspective, an authorized transaction occurred. Cold storage assets held by a regulated custodian like Coinbase Custody in a bankruptcy-remote structure offer meaningful protection against custodian insolvency, but that’s a structural protection, not an insurance payout. Before selecting a wallet based on insurance coverage, businesses should request the actual policy terms and have a qualified insurance professional review what is and isn’t covered under the specific loss scenarios they’re most concerned about.

Which of the Top 5 Wallets Carry Insurance Protections

Of the five wallets reviewed, Coinbase Prime offers the most explicit and documented insurance coverage, crime insurance on hot wallet assets and a bankruptcy-remote cold storage structure that protects client funds in an insolvency scenario. Ledger Enterprise offers crime insurance through its enterprise agreements, with coverage terms that vary by contract size and jurisdiction. CoinsPaid carries operational insurance as part of its licensed payment processor status, though coverage specifics depend on the jurisdiction and the business agreement in place, and businesses should confirm current licensing and coverage terms directly given Estonia’s 2026 regulatory transition. Tangem and MetaMask Institutional, as self-custody solutions, do not carry custodial insurance by design, because the business holds its own keys, there is no custodian to insure. The tradeoff is that self-custody eliminates custodian risk entirely, which is a form of protection that no insurance policy can replicate.

Regulated Crypto Wallets: Compliance Without Complexity

Regulatory Status of the Top 5 Business Crypto Wallets (2026)

Tangem: Registered in Switzerland; compliant with Swiss financial regulations; no custodial license required as a self-custody hardware manufacturer.

MetaMask Institutional: Operates through Consensys, which maintains legal entities across multiple jurisdictions; compliance depends on the custodian integration chosen by the business.

Ledger Enterprise: Registered in France; operates under EU regulatory frameworks; not a regulated custodian but partners with regulated custodians for enterprise deployments.

CoinsPaid: Previously VASP-licensed in Estonia. Estonia’s legacy VASP regime sunset on July 1, 2026, and the company is transitioning to full MiCA CASP authorization under the EU’s new framework; current status should be independently verified before relying on it for compliance purposes.

Coinbase Prime: Operates under Coinbase Custody Trust Company, chartered by the New York Department of Financial Services (NYDFS); most heavily regulated option on this list.

Regulation in the crypto wallet space doesn’t mean the same thing across all five of these products. For custodial solutions like Coinbase Prime and CoinsPaid, regulation means the provider is licensed, supervised, and subject to ongoing compliance audits by a government authority. For self-custody tools like Tangem and MetaMask Institutional, regulation applies to the product manufacturer or software provider, not to the custody of your funds, because you hold your own keys and are therefore your own custodian.

This distinction matters operationally. A business using Coinbase Prime can point to a regulated custodian when asked by auditors or investors to demonstrate that its crypto holdings are held responsibly. A business using Tangem can point to its own internal controls and the hardware’s certified security architecture. Neither answer is wrong, they satisfy different audiences and different compliance frameworks.

For businesses operating under formal investment mandates, fiduciary obligations, or regulatory reporting requirements, think registered investment advisers, publicly traded companies, or licensed financial institutions, a regulated custodian like Coinbase Prime is often a requirement, not a preference. For businesses that primarily need to demonstrate sound treasury practices to internal stakeholders or tax authorities, self-custody with documented internal controls is increasingly accepted.

The important thing is that “regulated” is not synonymous with “safer.” A regulated custodian can still be hacked, can still face insolvency, and can still freeze withdrawals under regulatory pressure. Self-custody with proper hardware and governance eliminates those specific risks. The right answer depends on your regulatory environment, your stakeholder requirements, and your operational capacity to manage keys responsibly. For more insights, consider exploring the long-term investment potential of Bitcoin vs. Ethereum.

Key Regulations Businesses Must Consider in 2026

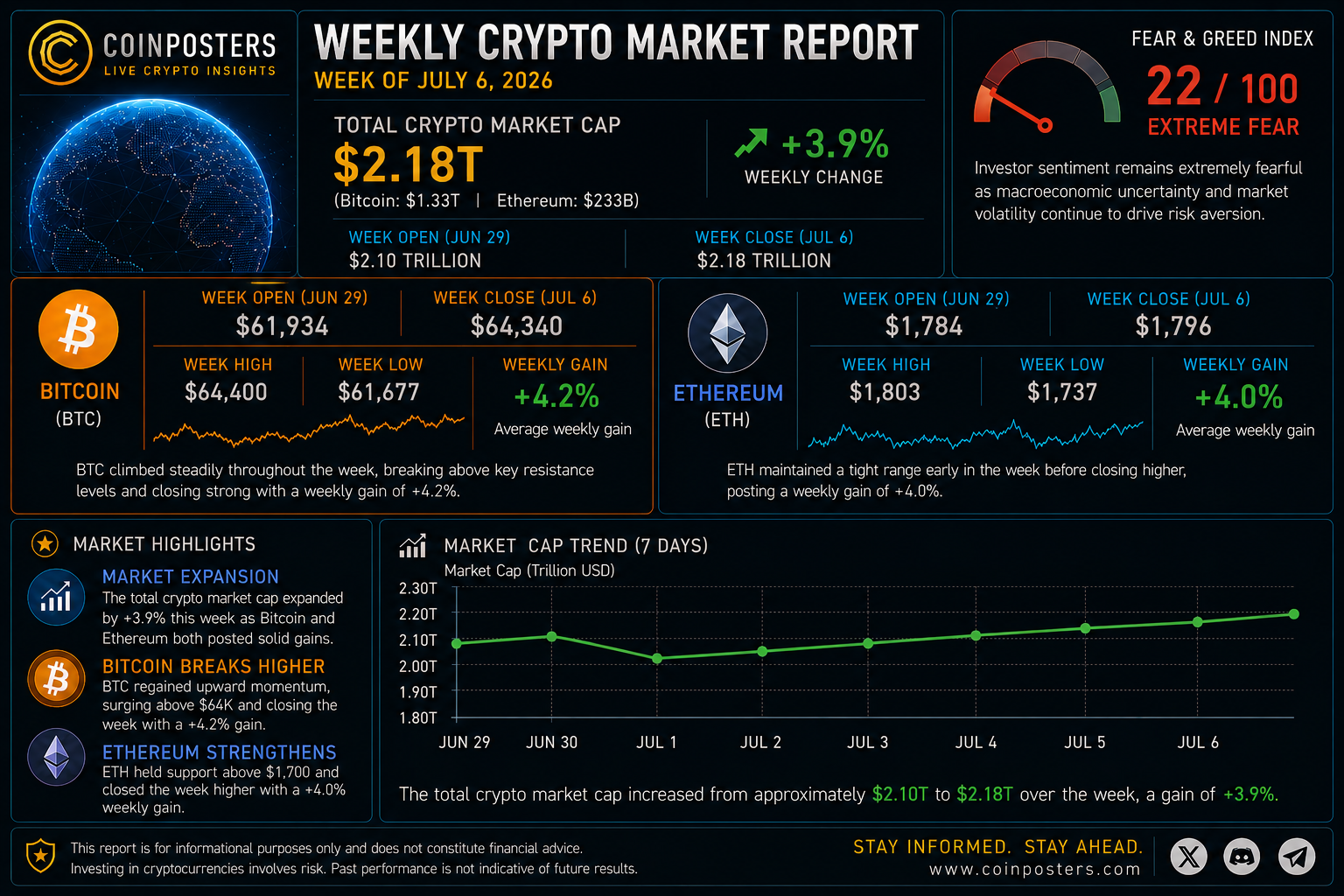

The regulatory landscape for crypto-holding businesses has shifted considerably. In the United States, the FASB’s updated accounting standards now require businesses to report crypto assets at fair value, with unrealized gains and losses flowing through the income statement, which means your wallet’s transaction history needs to be granular enough to support mark-to-market accounting. In the EU, the Markets in Crypto-Assets Regulation (MiCA) has introduced licensing requirements for crypto asset service providers and tightened AML obligations for businesses that transfer crypto, with a key transition deadline on July 1, 2026 that is actively reshaping which providers can legally continue serving EU clients. In the Asia-Pacific region, jurisdictions including Singapore, Hong Kong, and Australia have introduced or tightened VASP licensing frameworks that affect how businesses can legally hold and transfer digital assets. For any business operating across borders, the wallet solution needs to support the reporting and documentation requirements of every jurisdiction where the company has tax or regulatory obligations. For more insights on the evolving crypto landscape, you can read the crypto market report.

How Regulated Wallets Simplify Tax Reporting and Audits

The practical compliance advantage of using a purpose-built business wallet, regulated or otherwise, comes down to data quality. A wallet that generates structured, exportable transaction records with timestamps, counterparty addresses, asset types, and valuations dramatically reduces the manual work required at tax time. Coinbase Prime integrates directly with institutional-grade crypto tax platforms and generates the cost basis documentation that US institutional investors need for Schedule D reporting. CoinsPaid generates merchant transaction records that map to standard bookkeeping workflows. Ledger Enterprise exports transaction data in formats compatible with enterprise accounting systems. The alternative, manually reconciling transactions from a blockchain explorer against bank records, is not just inefficient; it’s a source of material errors that can create real tax liability or audit exposure.

Jurisdictional Differences That Affect Your Wallet Choice

A US-based business with no international operations has different wallet requirements than a global e-commerce platform processing payments in 40 countries. In the US, the primary compliance concerns are FASB accounting standards, IRS reporting, and FinCEN’s AML requirements for businesses that qualify as money services businesses. In the EU, MiCA compliance and GDPR implications for transaction data storage add additional layers. In jurisdictions without clear crypto regulation, which still describes a significant portion of the world, the priority shifts to demonstrating sound internal controls and maintaining clean records that can satisfy any future regulatory scrutiny. Your wallet choice should map to where your business actually operates and what documentation standard you’ll be held to.

Side-by-Side Comparison: Top 5 Business Crypto Wallets

| Wallet | Type | Self-Custody | Multi-User Access | Insurance | Regulated | Best Use Case |

|---|---|---|---|---|---|---|

| Tangem | Hardware (NFC Card) | Full | Multi-card | N/A (self-custody) | Switzerland-registered | Team treasury, self-custody, seedless security |

| MetaMask Institutional | Software + Custodian | Via custodian | Role-based | Varies by custodian | Custodian-dependent | DeFi access, Web3-native operations |

| Ledger Enterprise | Hardware + Platform | Full | Policy engine | Crime insurance | EU-registered | Large cold storage treasury |

| CoinsPaid | Custodial Payment Platform | Custodial | Team accounts | Operational | Transitioning to MiCA (verify current status) | Merchant payments, fiat settlement |

| Coinbase Prime | Custodial Institutional | Custodial | Role-based | Crime + cold storage | NYDFS chartered | Institutional custody, regulated trading |

How to Choose the Right Wallet for Your Business

The right business crypto wallet is determined by three factors: what you’re using crypto for, how many people need access, and what your compliance environment requires. A solo founder running a crypto-native startup has fundamentally different needs than the CFO of a publicly traded company with a Bitcoin treasury line item on the balance sheet. Getting this decision right means being honest about your actual use case rather than defaulting to whichever wallet has the most recognizable brand name.

Treasury Management vs. Payment Processing: Different Tools for Different Jobs

Treasury management and payment processing are distinct operational functions that require different wallet architectures. Treasury management is about long-term security, you need cold storage, approval workflows, audit trails, and the ability to demonstrate to auditors that funds are held responsibly with clear access controls. The priority is security over convenience, because treasury funds move infrequently but the consequences of a breach are severe.

Payment processing is about throughput and automation, you need fast transaction confirmation, real-time conversion, API connectivity to your checkout system, and reliable fiat settlement. The priority is operational efficiency over maximum security, because high-volume payment flows require automation that cold storage architectures aren’t built to support. Businesses that need both, a treasury reserve and active payment processing, should use separate tools for each function. Tangem or Ledger Enterprise for the treasury, CoinsPaid for the payment layer. Treating them as the same problem and reaching for a single tool to solve both is how businesses end up with the wrong wallet for at least one of those functions.

Matching Wallet Features to Your Team Size and Structure

Team size directly determines which wallet features matter most. A two-person founding team can manage a Tangem multi-card setup with both cards distributed between co-founders, simple, secure, and no third-party dependency required. A ten-person finance team needs role-based permissions, transaction approval tiers, and audit trails that separate who can view, initiate, and approve transactions. A fifty-person organization operating across multiple jurisdictions needs an enterprise platform with policy enforcement at the hardware or smart contract level, formal custodian agreements, and integration with the company’s existing ERP and accounting systems. Don’t pay for enterprise complexity you don’t need, but don’t underinvest in governance features that your team size requires. The cost of a governance failure, an unauthorized transfer, an internal fraud event, a lost seed phrase, will always exceed the cost of a proper business wallet setup.

Questions Every CFO Should Ask Before Committing to a Wallet

Before signing a contract or completing a wallet setup, every CFO responsible for business crypto assets should be able to answer these questions about their chosen solution, including whether a hot or cold wallet is the best option for their security needs:

- Who holds the private keys, and what happens to fund access if that person or entity becomes unavailable?

- How many approvals are required to execute a large outgoing transfer, and can that requirement be bypassed by any single party?

- What transaction data does the wallet export, and is it compatible with our accounting and tax reporting systems?

- If the wallet provider goes out of business, can we still access our funds independently?

- What does the insurance cover specifically, and have we reviewed the actual policy terms?

- Does this wallet satisfy the custody requirements of our investors, auditors, or regulators?

If any of these questions don’t have a clear answer before committing to a wallet, that’s the gap that needs to be closed first. A wallet decision made without answers to these questions is a governance risk, regardless of how good the underlying technology is.

Tangem Is the Strongest All-Around Business Wallet for Most Companies

For the majority of businesses, those that need self-custody, team access, broad chain support, and a security architecture that doesn’t depend on a seed phrase surviving intact, Tangem is the most complete solution available in 2026. The EAL6+ certified hardware, multi-card governance model, 90+ chain support, and seedless design address the specific failure modes that make consumer wallets dangerous for business use, without requiring the enterprise infrastructure overhead of a Ledger Enterprise or Coinbase Prime deployment. Businesses with specialized needs, regulated institutional custody, high-volume payment processing, or deep DeFi integration, should layer in the specialist tools designed for those functions. But as the foundation of a business crypto setup, Tangem hits the right balance of security, operational simplicity, and team access control that most companies actually need. For a deeper understanding of wallet security, consider exploring the differences between hot and cold wallets.

Frequently Asked Questions

Business crypto wallet questions tend to cluster around the same core concerns: security, team access, compliance, and how hardware compares to software. The answers below address the most common questions finance leaders and business owners ask when evaluating wallet options for the first time.

The right answer to most of these questions depends on your specific business context, but the frameworks below give you a starting point for thinking through each decision correctly.

What Is the Safest Crypto Wallet for a Small Business?

The safest crypto wallet for a small business is one that combines hardware-level key security with a backup system that doesn’t depend on a single seed phrase. Tangem’s multi-card setup is the strongest option for most small businesses, the EAL6+ certified chip means private keys are generated and stored on the physical card and cannot be extracted, while the multi-card architecture means no single lost or damaged card results in permanent fund loss. For small businesses that also need regulated custody, for example, because investors or auditors require it, Coinbase Prime offers the strongest regulatory standing of any option on this list, though it comes with the tradeoff of third-party custody rather than direct key control.

Do Business Crypto Wallets Require KYC Verification?

It depends entirely on the wallet type. Self-custody hardware wallets like Tangem and Ledger Enterprise do not require KYC verification because you are your own custodian, there is no regulated financial institution in the custody chain that is obligated to verify your identity. Custodial platforms like Coinbase Prime and CoinsPaid do require business KYC verification, typically including business registration documents, beneficial ownership information, and in some cases AML compliance documentation. For businesses in regulated industries or jurisdictions with strict VASP requirements, the KYC process for custodial wallets can be detailed, but it’s a one-time onboarding requirement rather than an ongoing operational burden.

Can a Business Wallet Support Multiple Employees With Different Access Levels?

Yes, but only if the wallet was designed for business use from the ground up. Tangem supports multi-user access through its multi-card architecture, where different cards can be distributed to different team members. MetaMask Institutional, Ledger Enterprise, and Coinbase Prime all offer role-based permission systems that let administrators assign different capabilities to different users, view-only access for bookkeepers, transaction initiation for finance managers, and final approval authority for executives. Consumer wallets like standard MetaMask or Trust Wallet have no native multi-user access capabilities, adding more than one user to a consumer wallet means sharing a single private key or seed phrase, which is a significant security vulnerability and should never be done with business funds. For more on wallet security, check out this comparison of hot wallets vs cold wallets.

What Is the Difference Between an Insured and a Regulated Crypto Wallet?

An insured wallet carries a specific insurance policy that pays out in the event of defined loss scenarios, typically third-party theft or physical breach of hardware storage. A regulated wallet is provided by a company that operates under a government-issued license and is subject to ongoing compliance supervision by a financial regulator. These are completely different things, and having one does not imply having the other.

Coinbase Prime is both insured and regulated, it operates under an NYDFS charter and carries crime insurance on hot wallet assets. CoinsPaid was previously licensed as a VASP in Estonia and carries operational insurance, though that licensing status is currently in transition following Estonia’s 2026 shift to full MiCA authorization and should be independently confirmed. Tangem is neither insured nor regulated in the custodial sense, because it’s a self-custody tool, you are the custodian, and the protection comes from the hardware security architecture rather than a financial institution’s compliance framework. Understanding this distinction is critical when evaluating wallets for compliance or investor relations purposes, because auditors and institutional investors may require regulated custody specifically, and hardware security, however strong, doesn’t satisfy that requirement on its own.

Is a Hardware Wallet or a Software Wallet Better for Business Treasury Management?

For treasury management, holding significant crypto reserves long-term, hardware wallets are the stronger choice in almost every scenario. The core reason is that hardware wallets store private keys on a physically isolated chip that never connects to the internet. Software wallets, regardless of how well-secured the application is, store keys in an environment that is connected to the internet and therefore exposed to remote attack vectors including malware, phishing, and application vulnerabilities.

The practical security gap between hardware and software wallets is largest precisely when the stakes are highest, large balances held over extended periods. A software wallet that handles routine operational payments is a reasonable operational tool. A software wallet holding your entire company treasury is a risk that hardware architecture eliminates for a comparatively small cost.

The operational argument for software wallets, that they’re faster and easier to use, is valid for payment processing workflows where transaction speed matters. It’s not a compelling argument for treasury storage, where transactions are infrequent and the priority is protecting assets that may not move for weeks or months at a time.

The best approach for most businesses is to use both: a hardware wallet like Tangem for treasury reserves and a software or payment platform like CoinsPaid for operational payment flows. This separation keeps the majority of company funds in cold storage while maintaining the transaction throughput needed for day-to-day operations, without requiring a single tool to do both jobs well simultaneously.

DYOR Disclaimer

This article is for informational purposes only and does not constitute financial, legal, or compliance advice. Regulatory status, licensing, and insurance coverage for the wallets discussed can change, always verify current terms directly with each provider and consult a qualified legal or compliance professional before making treasury decisions. Always do your own research (DYOR).