cryptocurrency yields

DeFi protocol risks

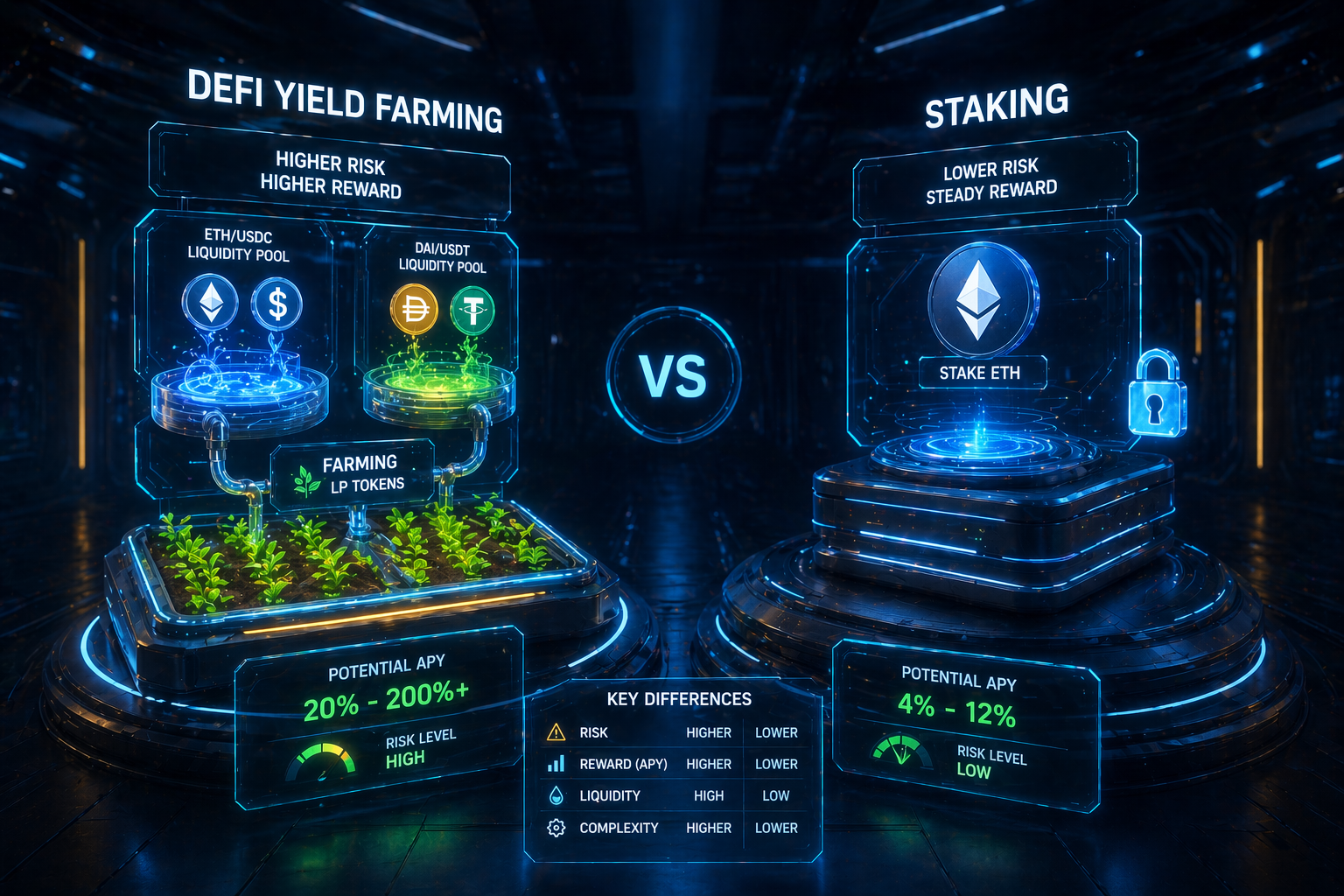

DeFi yield farming vs traditional savings

FDIC insurance protection

high yield savings accounts

impermanent loss risks

liquidity provider rewards

passive income strategies

smart contract vulnerabilities

stablecoin farming strategies

traditional banking alternatives

yield farming returns 2026

Coinposters

DeFi Yield Farming vs Traditional Savings | Which One is More Profitable for the Average Investor?

DeFi Strategies · Yield Comparison · Investment Returns · 2026 Guide

Traditional savings accounts barely offer 0.38% APY while DeFi yield farming promises returns exceeding 100%—but there’s a catch most investors miss. Before chasing those eye-popping yields, you need to understand what could wipe out your gains overnight.

Key Takeaways

- •DeFi yield farming offers 5-100%+ APY compared to traditional savings’ 0.38% average, but comes with significantly higher risks

- •Traditional savings provide FDIC insurance up to $250,000, while DeFi protocols face smart contract vulnerabilities and potential rug pulls

- •High-yield savings accounts now offer up to 5.00% APY, creating a middle-ground option for yield-seeking investors

- •Market conditions determine which strategy performs better, with bull markets favoring DeFi and bear markets making traditional savings safer

- •Active management requirements differ drastically between set-and-forget traditional accounts and constant DeFi monitoring

Table of Contents

- DeFi Yield Farming Can Offer 5-100%+ APY While Traditional Savings Average 0.38%

- Real Returns: What You Actually Earn From Each Strategy

- Hidden Costs That Eat Into Your Profits

- Risk Analysis: Security vs Potential Losses

- Active Management Requirements for Maximum Profitability

- Market Conditions Impact Which Strategy Wins

- Choose DeFi for Higher Returns or Traditional for Capital Preservation

The search for higher returns has led investors to compare the explosive growth potential of decentralized finance against the steady reliability of traditional banking. While both strategies aim to grow wealth through interest and yields, they operate in completely different risk environments with vastly different return potentials. Understanding DeFi yield farming vs traditional savings is critical for making informed investment decisions in 2026.

DeFi Yield Farming Can Offer 5-100%+ APY While Traditional Savings Average 0.38%

The numbers tell a striking story about the yield gap between traditional and decentralized finance. Traditional savings accounts currently average just 0.38% APY across major U.S. banks, barely keeping pace with inflation. Meanwhile, DeFi yield farming protocols routinely advertise annual percentage yields ranging from 5% for conservative stablecoin strategies to over 100% for high-risk liquidity provision.

This dramatic difference stems from how each system generates returns. Traditional banks profit by lending depositor funds at higher rates than they pay savers, keeping the spread as profit. Coinposters tracks the latest developments in yield-generating opportunities, showing how DeFi protocols instead distribute trading fees, governance tokens, and protocol incentives directly to liquidity providers.

0.38%

Average traditional savings APY

5-100%+

DeFi yield farming APY range

5.00%

High-yield savings accounts (up to)

“The catch lies in understanding what drives these elevated returns. DeFi yields often include temporary token incentives designed to bootstrap new protocols, creating unsustainable rate environments that can collapse rapidly.”

Smart yield farmers recognize when rates seem too good to be true and adjust their strategies accordingly. Understanding DeFi yield farming fundamentals helps investors distinguish between sustainable yields and temporary promotional rates.

Real Returns: What You Actually Earn From Each Strategy

Traditional Savings Interest Rates Hit Historic Lows

Federal Reserve monetary policy has created a dynamic environment for traditional savings rates over the past decade. Major banks like Wells Fargo and Bank of America offer standard savings rates below 0.50% APY, with some accounts paying as little as 0.01%. Recent years have seen rate increases followed by cuts in late 2024 and 2025, with projected cuts continuing in 2026. Most traditional accounts fail to provide meaningful wealth growth after accounting for inflation and taxes.

This environment has pushed savers to seek alternatives, but traditional banking maintains its appeal through predictable, guaranteed returns. Unlike DeFi protocols that can experience sudden rate changes or platform failures, traditional savings provide steady (albeit minimal) income with full principal protection.

High-Yield Savings Accounts (HYSAs) Offer Up to 5.00% APY Currently

Online banks and credit unions have emerged as a middle ground, offering high-yield savings accounts with rates up to 5.00% APY as of April 2026, with some standard savings accounts offering as high as 5.84% APY. These accounts combine FDIC insurance protection with yields that actually compete with inflation, making them attractive for emergency funds and conservative investors.

Popular HYSA providers like Marcus by Goldman Sachs, Ally Bank, and Capital One maintain competitive rates by operating with lower overhead costs than traditional brick-and-mortar institutions. The trade-off often involves limited branch access and fewer banking services, but the yield advantage can be substantial for passive savers.

| Account Type | Typical APY Range | Risk Level | Insurance/Protection |

|---|---|---|---|

| Traditional Savings | 0.01% – 0.50% | Very Low | FDIC up to $250,000 |

| High-Yield Savings | 4.00% – 5.84% | Very Low | FDIC up to $250,000 |

| Stablecoin Farming | 5% – 15% | Medium | None |

| DeFi Yield Farming | 10% – 100%+ | High to Very High | None |

DeFi Yield Farming APYs Range From 5% to Over 100% With Increased Risk

Decentralized finance protocols generate yields through multiple revenue streams that traditional banks cannot access. Liquidity providers on platforms like Uniswap and Curve earn trading fees, governance tokens, and protocol incentives that can compound into impressive annual returns. Stablecoin farming strategies typically offer 3-15% APY with lower volatility risk, while exotic token pairs can exceed 100% APY during promotional periods.

The sustainability of these yields depends heavily on platform adoption, token economics, and market conditions. Established protocols with proven track records tend to offer more conservative but reliable returns, while newer platforms use high yields to attract initial liquidity before rates normalize. Learning how yield farming works helps investors evaluate which opportunities are sustainable versus speculative.

Hidden Costs That Eat Into Your Profits

Both traditional and DeFi strategies involve costs that impact real returns. Traditional savings may include monthly maintenance fees, minimum balance requirements, and early withdrawal penalties that reduce effective yields. High-yield accounts sometimes impose rate tiers or promotional periods that decrease returns over time.

Hidden Costs That Reduce Your Actual Returns

Traditional Savings Costs:

- Monthly maintenance fees ($5-$15/month)

- Minimum balance requirements

- Early withdrawal penalties

- Rate tier reductions after promotional periods

DeFi Farming Costs:

- Blockchain gas fees (variable, historically $0.50-$196 per transaction)

- Token swap fees (0.05%-1% per trade)

- Reward claiming transaction costs

- Impermanent loss (can exceed all earned yields)

DeFi farming faces different cost structures, primarily through blockchain transaction fees (gas costs). While historical peaks for Ethereum gas fees reached up to $196 per transaction in May 2021, current average gas fees in April 2026 are significantly lower, often ranging from cents to a few dollars, though fees can still be volatile during network congestion. Smart contract interactions, token swaps, and reward claiming all require fees that eat into profits, especially for smaller investment amounts. Successful yield farmers calculate these costs before entering positions to ensure profitability.

Risk Analysis: Security vs Potential Losses

FDIC Insurance Protects Traditional Savings Up to $250,000

The Federal Deposit Insurance Corporation provides protection for traditional savings account holders, covering up to $250,000 per depositor, per bank, for each account ownership category. This insurance protects against bank failures, fraud, and operational losses, essentially eliminating principal risk for most savers. Even during economic crises, FDIC-insured deposits remain accessible and fully protected.

This safety net creates a risk-free foundation for emergency funds and conservative portfolio allocations. Investors can confidently park substantial sums in traditional accounts without worrying about principal loss, making them ideal for short-term financial goals and capital preservation strategies.

“Decentralized finance operates without traditional safety nets, exposing users to smart contract bugs, protocol exploits, and malicious developers. Smart contracts containing millions of dollars can be drained through code vulnerabilities, as seen in numerous high-profile hacks across DeFi history.”

DeFi Risks Include Smart Contract Vulnerabilities and Rug Pulls

Decentralized finance operates without traditional safety nets, exposing users to smart contract bugs, protocol exploits, and malicious developers. Smart contracts containing millions of dollars can be drained through code vulnerabilities, as seen in numerous high-profile hacks across DeFi history. Even audited protocols face risks from complex interactions and unforeseen edge cases.

Rug pulls represent another significant threat, where project developers abandon protocols or extract user funds through backdoors. Research shows DeFi protocols experienced substantial increases in illicit activity, highlighting the importance of due diligence when selecting farming opportunities. New protocols with unproven teams pose the highest risk for these exit scams.

| Risk Type | Traditional Savings | DeFi Yield Farming |

|---|---|---|

| Principal Loss | Protected by FDIC ($250K) | No protection |

| Platform Failure | Insured against bank collapse | Total loss possible |

| Smart Contract Risk | None | Bugs can drain funds |

| Fraud/Rug Pulls | Extremely rare, insured | Common in new protocols |

| Volatility Risk | None (USD-denominated) | High (crypto exposure) |

| Impermanent Loss | Not applicable | Can exceed all yields |

Impermanent Loss Can Wipe Out Yield Farming Gains

Liquidity providers face a unique risk called impermanent loss when token prices diverge from their initial ratio. If one token in a liquidity pair significantly outperforms the other, providers may end up with fewer total assets than if they had simply held the tokens separately. This mathematical consequence of automated market maker mechanics can eliminate yield farming profits entirely during volatile market periods.

Impermanent loss becomes “permanent” when liquidity providers withdraw their positions at unfavorable price ratios. Experienced farmers minimize this risk by choosing correlated token pairs, using single-asset staking strategies, or selecting protocols with impermanent loss protection mechanisms. Resources like detailed yield farming guides explain these complex mechanisms in practical terms.

Active Management Requirements for Maximum Profitability

Traditional Savings: Set and Forget Approach

Traditional savings accounts require minimal ongoing attention once established. Account holders can automate deposits, let compound interest work over time, and focus on other financial priorities. Rate changes happen gradually and are communicated in advance, allowing savers to make informed decisions about account switches without time pressure.

The simplicity of traditional savings makes them accessible to investors of all experience levels. No technical knowledge, market timing, or platform monitoring is required to maintain steady returns. This passive approach suits busy professionals, retirees, and anyone who prefers hands-off investment strategies.

Time Investment Required for Each Strategy

Traditional Savings Management:

- Initial setup: 15-30 minutes

- Ongoing monitoring: 5 minutes quarterly

- Rate shopping: 1-2 hours annually

- Total annual time: 2-3 hours

DeFi Yield Farming Management:

- Initial research and setup: 5-10 hours

- Daily monitoring: 15-30 minutes

- Position rebalancing: 2-4 hours monthly

- Total annual time: 150+ hours

Yield Farming Demands Constant Platform Monitoring

Successful yield farming requires active engagement with rapidly changing DeFi markets. Farmers must track yield rates across multiple protocols, monitor token prices for impermanent loss risks, and stay informed about protocol updates, governance changes, and security developments. High yields can disappear overnight as incentive programs end or liquidity migrates to more attractive opportunities.

Platform monitoring extends beyond simple rate comparisons. Farmers need to evaluate smart contract audits, assess development team credibility, and understand tokenomics that drive yield sustainability. Gas fee optimization, reward claiming strategies, and position rebalancing all require ongoing attention to maximize returns.

Market Conditions Impact Which Strategy Wins

Bull Markets Can Amplify DeFi Returns But Increase Volatility Risks

Rising cryptocurrency markets create favorable conditions for DeFi yield farming through multiple channels. Token appreciation boosts the value of farming rewards, increased trading volume generates higher fee revenue for liquidity providers, and new protocol launches offer attractive incentive programs. During bull runs, successful farmers can achieve returns that far exceed traditional investments.

However, bull markets also intensify volatility risks that can quickly reverse gains. Rapid price movements increase impermanent loss potential, overheated markets become susceptible to sharp corrections, and speculative farming opportunities often prove unsustainable. Smart farmers take profits during favorable conditions rather than assuming bull markets will continue indefinitely.

Bull Market Advantages

DeFi: Token appreciation, high trading fees, new protocols

Traditional: Stable but unchanged returns

Bear Market Advantages

DeFi: Compressed yields, protocol failures, high risk

Traditional: Capital preservation, potential rate increases

Bear Markets Make Traditional Savings Safer

Economic uncertainty and falling cryptocurrency prices shift the risk-reward balance toward traditional savings. Market stress tests reveal which DeFi protocols survive and which collapse under pressure, while traditional banks continue operating regardless of crypto market conditions. During bear markets, capital preservation often takes priority over yield optimization.

Bear market conditions also compress DeFi yields as trading volumes decline, protocol incentives decrease, and risk appetites diminish. Traditional savings rates may actually increase during these periods as central banks raise interest rates to combat inflation, creating more competitive yield environments for conservative investors.

Stablecoin Farming Bridges Both Strategies

Stablecoin yield farming offers a compromise between traditional savings safety and DeFi return potential. By farming with USD-pegged tokens like USDC, DAI, or USDT, investors can access DeFi yields while minimizing cryptocurrency volatility exposure. Popular stablecoin farming strategies on platforms like Curve and Aave typically offer 5-15% APY with relatively stable principal values.

This approach combines DeFi protocol risks with reduced price volatility, creating a middle ground for yield-seeking investors. While still subject to smart contract risks and platform failures, stablecoin farming eliminates the impermanent loss concerns associated with volatile token pairs, making it more accessible for conservative investors exploring DeFi opportunities.

Stablecoin Farming as a Middle-Ground Strategy

Advantages:

- Higher yields than traditional savings (5-15% APY)

- Minimal cryptocurrency price volatility

- No impermanent loss in single-asset strategies

- Dollar-denominated returns similar to traditional accounts

Risks:

- Smart contract vulnerabilities remain

- Stablecoin depeg risk (historically rare but possible)

- No FDIC or government insurance

- Platform and protocol failure risks

Choose DeFi for Higher Returns or Traditional for Capital Preservation

The choice between DeFi yield farming vs traditional savings ultimately depends on individual risk tolerance, investment goals, and market outlook. Investors prioritizing capital preservation and guaranteed returns should anchor their strategies in FDIC-insured accounts, using high-yield savings options to maximize traditional returns while maintaining full principal protection.

Risk-seeking investors comfortable with cryptocurrency volatility and smart contract risks can explore DeFi farming opportunities for potentially superior returns. The key lies in proper risk management through diversification, protocol due diligence, and position sizing that won’t jeopardize overall financial stability. Many successful investors use both strategies, maintaining emergency funds in traditional accounts while allocating speculative capital to DeFi opportunities.

Decision Framework: Which Strategy Fits Your Goals?

Choose Traditional Savings If:

- Capital preservation is your priority

- You need guaranteed, stable returns

- Emergency fund or short-term goals

- Low risk tolerance

- Prefer hands-off management

Choose DeFi Yield Farming If:

- Seeking maximum return potential

- Comfortable with high volatility

- Can actively monitor positions

- Understand technical risks

- Capital you can afford to lose

Consider Stablecoin Farming If:

- Want higher yields than traditional

- Prefer minimal price volatility

- Willing to accept protocol risks

- Dollar-denominated returns preferred

- Bridge between both strategies

Market timing also influences strategy selection, with traditional savings providing stability during uncertain periods and DeFi farming offering growth potential during favorable market conditions. The most effective approach often involves dynamic allocation between strategies based on changing market environments and personal financial circumstances.

For investors seeking to stay informed about the evolving landscape of yield-generating opportunities across both traditional and decentralized finance, visit Coinposters for expert analysis and market insights.

DYOR (Do Your Own Research)

This article is for informational purposes only and does not constitute financial, investment, or tax advice. DeFi yield farming involves significant risks including total loss of capital through smart contract vulnerabilities, protocol failures, impermanent loss, and market volatility. Traditional savings accounts offer FDIC insurance but may not keep pace with inflation. APY rates mentioned are estimates and projections for 2026 based on current trends and may vary significantly. Past performance does not guarantee future results. Always conduct thorough research, understand the risks involved, and consider consulting with qualified financial advisors before making investment decisions. Coinposters provides educational content only and is not responsible for individual investment outcomes or losses.

Latest

Markets

08 Jul 2026

Markets

04 Jul 2026